By 2030, ten powerful converging technologies will entirely transform the way businesses work and engage with their customers. Here’s what you need to know:

Artificial Intelligence

Software algorithms that automate complex decision-making tasks to mimic human thought processes and senses. AI will exponentially speed up every aspect of human and machine interaction.

What is Artificial Intelligence

Artificial Intelligence is the combination of algorithms used to create intelligent machines. It is said that the next great leap in technology will not be systems that run faster and more efficiently, but rather a platform capable of anticipating our every need which is the foundation successful businesses are built upon.

Augmented Reality

Augmented Reality or AR as it’s fondly called is a visual or audio “overlay” on the physical world that uses contextualized digital information to augment the user’s real-world view.

It will be used to inform and amplify your interaction with all aspects of your everyday life, work and travel. Companies like Apple have already positioned themselves for the future with the design of the Apple Glass. The purpose of the Glass is to bring all of the information from your phone directly to your face.

AR will turn your gaze on almost anything in your surroundings, squint thoughtfully, and immediately view informational content about the object or activity of focus. Imagine the power it will give any businesses that adopt this technology now.

Virtual Reality

VR is an interface in which viewers can use special equipment to interact with a three-dimensional computer-generated simulation in realistic ways. Unlike AR which adds digital elements to a live view often by using the camera on a smartphone, VR is a complete immersion experience that shuts out the physical world.

The adoption of VR is poised to bring transformation to businesses that operate in the sphere of education, entertainment, medicine and more.

3D Printing

3D Printing is a machine that creates three-dimensional objects based on digital models by layering or “printing” successive layers of materials. It is used to fabricate bespoke ‘everything’ from homes and automobile parts to the replacement of human bio-tissues.

3D printing tech has brought massive innovation to the world. The technology has its imprint on virtually all industries. it is a sure-fire for any business to last the mile.

Internet of Things

IoT, as it is often called, is a network of physical objects embedded with sensors, software, network connectivity and computing capability, and can collect, exchange and act on data.

The Internet of Things has already started to revolutionize our homes and workplaces with smart speakers, lights and heating thereby minimising and simplifying everyday decision-making.

Robotics

Robotics is the use of machines with enhanced sensing, control and intelligence to automate, augment or assist human activities. Robotics tech is already in use in different industries like healthcare, education, manufacturing and research institutions.

Read More: 21 Digital Tools To Use For Your Business In 2022.

Quantum Computing

Quantum Computing is a new generation of technology of advanced computers 158 million times faster than the most sophisticated supercomputer. It will comfortably do in 4 minutes what it would take a traditional supercomputer 10,000 years to accomplish.

This technology holds the potential to transform medicine, create unbreakable encryption and even teleport information. Any business with the ability to integrate Quantum Computer will easily dominate its industry for years to come.

Gene Editing

Gene Editing is a group of technologies that give scientists the ability to change an organism’s DNA by allowing genetic material to be added, removed or altered at particular locations in the genome. This technology possesses the capability to extend the human life span and improve health and quality of life.

Already, scientists are making precise edits to DNA strands, leading to treatments for genetic diseases. This is a game-changer for the healthcare industry.

The use of Gene Editing tech could potentially push any company to the pinnacle of domination.

Materials Science

Material Science is the discovery and development of new materials accelerated by the Materials Genome Initiative. It allows scientists to create new elements and better products, transforming many aspects of everyday life.

Blockchain Technology

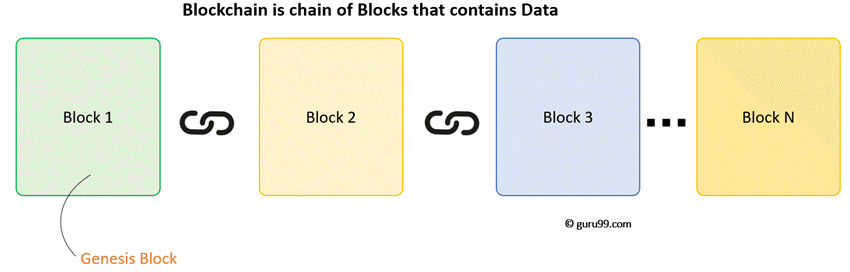

You are already familiar with Blockchain Technology based on previous articles we’ve written on it. But in case you need a rehash, Blockchain Technology is a distributed digital ledger that uses software algorithms to record and confirm transactions with reliability and anonymity.

The technology creates the infrastructure for web3 and transforms the internet — returning power and ownership to individuals.

READ: 21 Digital Tools To Use For Your Business In 2022.

Already, Blockchain Technology is disrupting the financial industries as more people are adopting the use of the technology – based on its most singular significant feature of decentralisation – to perform payment transactions with ease.

Any payment platform that wishes to stay relevant should start thinking of ways to integrate the use of Blockchain Technology.

Conclusion

That’s it! These are the 10 Most Powerful Business Technologies you need to start adopting right now as a business owner if you don’t want your business to be swept away by the rising current of innovations out there.